Window Functions - Rolling and Expanding Metrics

A Summary of lecture "Manipulating Time Series Data in Python", via datacamp

- Rolling window function with pandas

- Expanding window functions with pandas

- Case study: S&P500 price simulation

- Relationships between time series: correlation

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

plt.rcParams['figure.figsize'] = (10, 5)

Rolling average air quality since 2010 for new york city

The last video was about rolling window functions. To practice this new tool, you'll start with air quality trends for New York City since 2010. In particular, you'll be using the daily Ozone concentration levels provided by the Environmental Protection Agency to calculate & plot the 90 and 360 day rolling average.

data = pd.read_csv('./dataset/ozone_nyc.csv', parse_dates=['date'], index_col='date')

print(data.info())

# Calculate 90d and 360d rolling mean for the last price

data['90D'] = data['Ozone'].rolling('90D').mean()

data['360D'] = data['Ozone'].rolling('360D').mean()

# Plot data

data.loc['2010':].plot(title='New York City');

Rolling 360-day median & std. deviation for nyc ozone data since 2000

The last video also showed you how to calculate several rolling statistics using the .agg() method, similar to .groupby().

Let's take a closer look at the air quality history of NYC using the Ozone data you have seen before. The daily data are very volatile, so using a longer term rolling average can help reveal a longer term trend.

You'll be using a 360 day rolling window, and .agg() to calculate the rolling mean and standard deviation for the daily average ozone values since 2000.

data = pd.read_csv('./dataset/ozone_nyc.csv', parse_dates=['date'], index_col='date').dropna()

# Calculate the rolling mean and std here

rolling_stats = data['Ozone'].rolling(360).agg(['mean', 'std'])

# Join rolling_stats with ozone data

stats = data.join(rolling_stats)

# Plot data

stats.plot(subplots=True);

Rolling quantiles for daily air quality in nyc

You learned in the last video how to calculate rolling quantiles to describe changes in the dispersion of a time series over time in a way that is less sensitive to outliers than using the mean and standard deviation.

Let's calculate rolling quantiles - at 10%, 50% (median) and 90% - of the distribution of daily average ozone concentration in NYC using a 360-day rolling window.

data = data.resample('D').interpolate()

print(data.info())

# Create the rolling window

rolling = data['Ozone'].rolling(360)

# Insert the rolling quantiles to the monthly returns

data['q10'] = rolling.quantile(0.1).to_frame('q10')

data['q50'] = rolling.quantile(0.5).to_frame('q50')

data['q90'] = rolling.quantile(0.9).to_frame('q90')

# Plot the data

data.plot()

Expanding window functions with pandas

- Expanding windows in pandas

- From rolling to expanding windows

- Calculate metrics for periods up to current date

- New time series reflects all historical values

- Useful for running rate of return, running min/max

- Two options with pandas:

.expanding()-

.cumsum(),.cumprod(),.cummin(),.cummax()

- How to calculate a running return

- Single period return $r_t$: current prince over last price minus 1: $$ r_t = \frac{P_t}{P_{t-1}} - 1 $$

- Multi-period return: product of ($1 + r_t$) for all periods, minus 1: $$ R_T = (1 + r_1)(1 + r_2) \dots (1 + r_T) - 1 $$

Cumulative sum vs .diff()

In the video, you have learned about expanding windows that allow you to run cumulative calculations.

The cumulative sum method has in fact the opposite effect of the .diff() method that you came across in chapter 1.

To illustrate this, let's use the Google stock price time series, create the differences between prices, and reconstruct the series using the cumulative sum.

data = pd.read_csv('./dataset/google.csv', parse_dates=['Date'], index_col='Date').dropna()

differences = data.diff().dropna()

# Select start price

start_price = data.first('D')

# Calculate cumulative sum

cumulative_sum = start_price.append(differences).cumsum()

# Validate cumulative sum equals data

print(data.equals(cumulative_sum))

data = pd.read_csv('./dataset/apple_google.csv', parse_dates=['Date'], index_col='Date')

investment = 1000

# Calculate the daily returns here

returns = data.pct_change()

# Calculate the cumulative returns here

returns_plus_one = returns + 1

cumulative_return = returns_plus_one.cumprod()

# Calculate and plot the investment return here

cumulative_return.mul(investment).plot();

Cumulative return on $ 1,000 invested in google vs apple II

Apple outperformed Google over the entire period, but this may have been different over various 1-year sub periods, so that switching between the two stocks might have yielded an even better result.

To analyze this, calculate that cumulative return for rolling 1-year periods, and then plot the returns to see when each stock was superior.

def multi_period_return(period_returns):

return np.prod(period_returns + 1) - 1

# Calculate daily returns

daily_returns = data.pct_change()

# Calculate rolling_annual_returns

rolling_annual_returns = daily_returns.rolling('360D').apply(multi_period_return)

# Plot rolling_annual_returns

rolling_annual_returns.mul(100).plot();

Case study: S&P500 price simulation

- Random walks & simulations

- Daily stock returns are hard to predict

- Models often assume they are random in nature

- Numpy allows you to generate random numbers

- From random returns to prices: use

.cumprod() - Two examples:

- Generate random returns

- Randomly selected actual SP500 returns

np.random.seed(42)

# Create random_walk

random_walk = np.random.normal(loc=0.001, scale=0.01, size=2500)

# Convert random_walk to pd.series

random_walk = pd.Series(random_walk)

# Create random_prices

random_prices = random_walk.add(1).cumprod()

# Plot random_prices

random_prices.mul(1000).plot();

Random walk II

In the last video, you have also seen how to create a random walk of returns by sampling from actual returns, and how to use this random sample to create a random stock price path.

In this exercise, you'll build a random walk using historical returns from Facebook's stock price since IPO through the end of May 31, 2017. Then you'll simulate an alternative random price path in the next exercise.

fb = pd.read_csv('./dataset/fb.csv', header=None, index_col=0)

fb.index = pd.to_datetime(fb.index)

fb.index = fb.index.rename('date')

fb.columns = ['price']

np.random.seed(42)

# Calculate daily_returns here

daily_returns = fb['price'].pct_change().dropna()

# Get n_obs

n_obs = daily_returns.count()

# Create random_walk

random_walk = np.random.choice(daily_returns, size=n_obs)

# Convert random_walk to pd.Series

random_walk = pd.Series(random_walk)

# Plot random_walk distribution

sns.distplot(random_walk);

random_walk = pd.read_csv('./dataset/random_walk.csv', header=None, index_col=0)

date_range = pd.date_range(start=fb.index[1], periods= len(fb) - 1, freq='B')

random_walk.index = date_range

random_walk = pd.Series(random_walk[1])

start = fb['price'].first('D')

# Add 1 to random walk and append to start

random_walk = random_walk.add(1)

random_price = start.append(random_walk)

# Calculate cumulative product here

random_price = random_price.cumprod()

# Insert into fb and plot

fb['random'] = random_price

fb.plot();

Relationships between time series: correlation

- Correlation & relations between series

- So far, focus on characteristics of individual variables

- Now: characheristic of relations between variables

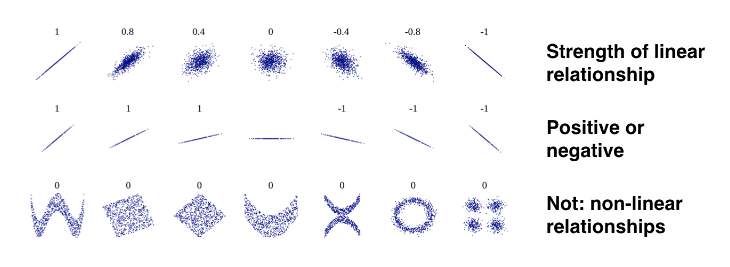

- Correlation: measures linear relationships

- Financial markets: important for prediction and risk management

- Correlation & linear relationships

- Correlation coefficient: how similar is the pairwise movement of two variables around their averages?

- Varies between $-1$ and $+1$:

$$ r = \frac{\sum_{i=1}^{N}(x_i - \bar{x})(y_i - \bar{y})}{s_x s_y} $$

Annual return correlations among several stocks

You have seen in the video how to calculate correlations, and visualize the result.

In this exercise, we have provided you with the historical stock prices for Apple (AAPL), Amazon (AMZN), IBM (IBM), WalMart (WMT), and Exxon Mobile (XOM) for the last 4,000 trading days from July 2001 until the end of May 2017.

You'll calculate the year-end returns, the pairwise correlations among all stocks, and visualize the result as an annotated heatmap.

data = pd.read_csv('./dataset/5_stocks.csv', parse_dates=['Date'], index_col='Date')

print(data.info())

# Calculate year-end prices here

annual_prices = data.resample('A').last()

# Calculate annual returns here

annual_returns = annual_prices.pct_change()

# Calculate and print the correlation matrix here

correlations = annual_returns.corr()

print(correlations)

# Visualize the correlations as heatmap here

sns.heatmap(correlations, annot=True);

plt.savefig('../images/stock_heatmap.png')